If you’re like me, you probably woke up one day to corners of the English lexicon that sounded downright fictional, or foreign at best. Crypto, bitcoin, de-fi, blockchain, NFTs, cryptokitties, and now metaverse. And if you’re really like me, it all felt so disconnected from the issues on our mind and heart these days that they didn’t seem worth worth more than a thumbscroll. All of the articles I’ve read, videos I’ve watched, and people I’ve spoken with, assumed a prerequisite understanding of software development and/or finance — neither of which I’ve studied at length. Their explanations expectedly went over my head, and my motivation to have a light bulb moment waned.

But eventually, the prevalence of these buzzwords didn’t seem to erode. In fact, they grew stronger over time as the issues we were managing began to increase in severity. And it’s this intersection of these trends and social justice that prompted me to prioritize understanding of these emerging concepts and the role they will play in our lives. This article is a primer for people like me who’ve failed numerous times to navigate the steep learning curve to understanding this new frontier. My goal is not to present expertise on any of these topics, but instead document my learnings as I work to understand what it all means for myself, my team, and our community. If anything is resonates, or is unclear/incorrect, hit me up on Twitter @zanders.

Blockchain

Throughout history, contracts have had to be executed manually, regardless of how form the relationship was. Two or more parties would have to physically sign that standard agreement as many times as the terms of the agreement changed, no matter how slightly. While digital signatures like Docusign have eased some of the friction involved, there are still barriers to contracts. This includes the affordability of legal counsel, the consequences of poor counsel, the time it takes to ensure accuracy, access and storage over time, and more. But what if the terms of a contract could be written into a software program with no room for error, rules on how to handle a multitude of scenarios, transparent and accessible storage, and the ability to be executed virtually?

These are some of the primary benefits of blockchain – a technology introduced in 2009 to make contracts and the ledger that maintains their record “smart”. A blockchain can be public or private (eg IBM provides blockchain services to enterprise businesses). The first blockchain created was for Bitcoin, which uses blockchain’s distributed trait to enable anyone to view the transactions that take place on the ledger. However, bitcoin and blockchain are not synonymous. More on this in the section on cryptocurrency.

There are thousands of blockchains today, a number that will continue growing over time. I could see a world where all of our transactions take place on one blockchain or another. You’ll start to hear about certain transactions taking place “on chain”, versus ones that take place off chain. “On chain” shouldn’t be conflated with transactions that take place online, which is also referred to as “e-commerce”. Technically, all on chain transactions take place online, but not all online transactions are on chain.

While smart contracts are a big step forward, there are downsides. The largest is how difficult smart contracts are to adopt as an individual or an organization. As a software program, software development expertise is required, along with onboarding to blockchain’s concepts to apply them to your use case. This has created high demand for both blockchain engineers and blockchain consultants, both of which will become jobs of the future in every university, library, and municipality over the next decade.

Decentralized Finance

The transparency, security, privacy, and reliability offered by blockchain has created radically new ways of thinking about day-to-day transactions, such as buying and selling goods and services. Because blockchain functions as a digital ledger governed by a software program as opposed to an institution, blockchain engineers are able to create new economic frameworks (think beyond capitalism or socialism) that serve as an alternative to ones controlled by a central government. This decentralized approach enables two or more parties to bypass a central agency (a federal reserve bank for example) to transact according to a set of previously agreed upon rules that have been written into the software program. It is considered incorruptible due to the removal of human decision making with regard to what transactions take place and which rules are applied and under what circumstances. Also referred to as “de-fi”, the movement risen in popularity around the world due to the growing skepticism towards a centralized approach to government.

Cryptocurrency

In a decentralized economy governed by a digital authority, two or more parties transacting need a new medium of exchange that can serve as a store of value. Back in the days of bartering, I would give you my sugar in exchange for your milk. But in this new digital economy, we need a currency that abides by the set of modern, pre-determined rules of transparency, security, privacy, and accessibility. Cryptocurrency, nicknamed “crypto”, is a form of currency that meets this criteria by leveraging cryptography principles. Rather than dollars, cryptocurrency is measured in “coins” — a form of “token” that can be valued based on two primary factors: scarcity and demand. This was an easier aspect for me to grasp, having grown up playing video games in arcades, needing to exchange dollars for tokens.

Aside from security, a defining factor of this new form of currency is that the number of coins is pre-set according to rules encoded in the smart contract on the blockchain. This manufactured scarcity helps people who hold the digital currency have confidence that it’s value won’t diminish due to “overprinting” or over-production. There are thousands of “coins” that have been created, each of which have a set number that can be “mined” according to the smart contract for the coin on the blockchain. To enter into circulation, the coins must be “mined” — a process that involves a person setting up a high performance computer typically used for activities like gaming, and configure it to solve mathematical puzzles to validate transactions on the blockchain. (Think of this like a more sophisticated version of the Captcha tests used to validate our humanity when logging into a website.) Mining can get expensive due to the specialized equipment, and also the amount of energy required to work through the amount of puzzles necessary to generate a profit.

For example, bitcoin, ethereum, guapcoin, and USD coin, are four different “coins,” similar to pesos, yen, or US dollars. But the number of each coin that is in circulation is communicated as the the plural of the name of the coin (eg bitcoins, guapcoins, USD coins). The most popular coin today is Bitcoin. Only 21 million bitcoins can enter into circulation. Because of the rapid adoption of bitcoin as an alternative store of value as opposed to cash, stocks or bonds, investors have driven the price of each bitcoin to $50,000.

Ethereum

As shown in the chart above, the second most popular cryptocurrency today is Ethereum. Ethereum, six years younger than Bitcoin, is its own public blockchain, but governed by different rules than Bitcoin. Like bitcoin, the ethereum blockchain has its own cryptocurrency, Ether coins. Ether coins are currently priced at almost $4,000 as of this writing. Unlike bitcoin there’s no limit to the number of Ether coins that can be minted. Instead, there’s an annual limit of 18 million per year. Beyond the currency, ethereum has developed a much more inclusive digital economy by providing tools manage any digital asset in a more secure and accessible way.

Decentralized Apps

Ethereum has accomplished this by enabling the development of software applications that leverage the blockchain and its principles of security, transparency, and privacy. I’ve come across ethereum-based publishing platforms for writers to earn revenue like Mirror.xyz, web browsers that promote privacy and prevent tracking like Brave, and even music sharing platforms that give artists 100% revenue in their music like Catalog. This new class of apps are referred to as Decentralized Apps, nicknamed “dApps”, because they are hosted on a distributed network of computers, each existing as a smart contract on the blockchain. While there are hundreds of dapps that have been created, I want to focus on a few key dapps for you to get started.

- Wallets

- Name Services

- Non-Fungible Tokens (NFTs)

Wallets

Similar to physical money, digital currency requires a container to hold it, which also functions as the mechanism to convert money into crypto, or exchange crypto with others. These containers, called wallets, also make the onboarding process to crypto simpler by creating a user interface to create an account that is associated with your email address. Crypto wallets can be downloaded on your mobile device like as a mobile (Rainbow.me), or installing a chrome extension your browser (Metamask). Both are storing your data in the cloud rather than locally on your device. After creating an account using your email address, your wallet of choice will create an unique alphanumeric address for you that is used to write transactions on your behalf to the blockchain. This long ID is hard to remember and easy to confuse. (Side note: I recommend adopting a password manager like 1Password before getting into crypto. If you already have issues keeping track of passwords, crypto will multiply your challenges here. And worse, you can lose a lot of money in the process.)

While you will have traditional login credentials (eg username/email, password, and recovery phrase) for your wallet app or browser extension, using dapps simply require you to connect your wallet. This is done by either scanning the dapp’s QR code with your wallet, or connecting through your browser extension. One thing to keep in mind is that only you should have access to your wallet. Your wallet connects to your bank account to transfer money into bitcoin or ether coins. These aren’t credentials you want to share with anyone else. It’s also worth noting that the same features that make blockchain so secure make it almost impossible to get access to a wallet once you lose your recovery phrase. So before you dive in, make sure you have the mental space to get organized. But once you do, there’s a whole world to explore.

Name Services

One of the first dapps that was built on the ethereum blockchain was a name service that offered a more user-friendly handle to replace the long alphanumeric wallet address. But these domains differ from a simple website domain because they have the ability to connect you to the blockchain. I used the Ethereum Name Service to create zanders.eth. This also comes in handy when receiving tokens from others. For example, you can see the different tokens I’ve chosen to showcase on this public URL for my wallet: rainbow.me/zanders.eth. This URL doesn’t display how much money I have in Ethereum, Bitcoin, or other tokens, but only a certain type of tokens that are unique or “non-fungible”.

Non-fungible Tokens (NFTs)

Tokens like a currency are not unique. As previously mentioned, the bitcoin smart contract limits total production to 21 million bitcoins. Ethereum’s smart contract does not cap the total number of ether coins that in circulation, but does cap the maximum amount minted per year to 18 million. But in 2018, ethereum developers made an update to the blockchain to recognize the uniqueness of a digital asset. These non-fungible tokens, better known as “NFTs” are what got me into this entire conversation.

The practical problem this solves is that we haven’t developed a reliable way to verify the uniqueness of digital assets (eg JPEGs, PDFs, PNGs, etc…) as we have for physical assets (eg books, paintings, photographs). But because of the blockchain’s public ledger for digital assets, each NFT has its own smart contract that confirms the owner, regardless of how many people have a copy of it.

Before NFTs, artists, authors, photographers, and other producers of digital assets have struggled to demonstrate ownership of their work online, and as a result, have difficulty to monetize their labor. If you take a moment to consider the implications here, they are really quite huge. While many NFTs are individual digital objects that were created outside of Ethereum and uploaded to an art marketplace like OpenSea to assign it a smart contract on the blockchain, the most popular NFTs are substantially different.

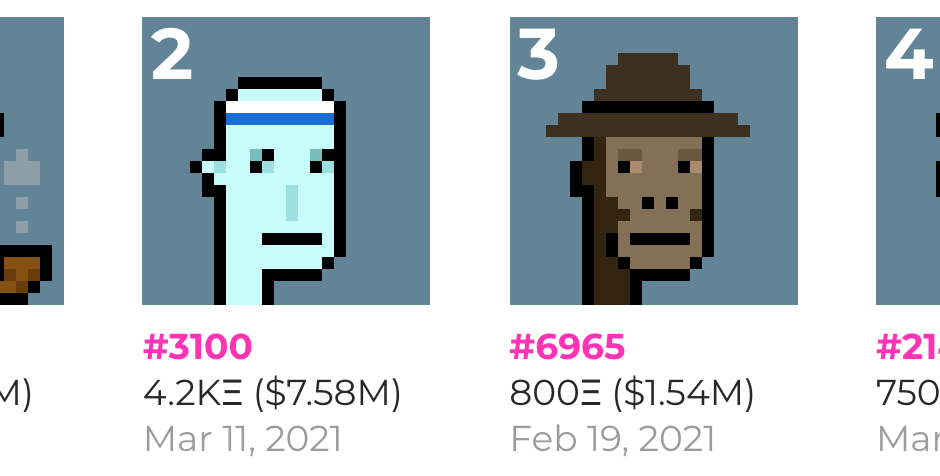

Take the popular CryptoPunks for example. A software company that specializes in blockchain called Larva Labs wrote a dapp on the ethereum blockchain that dynamically generated 10,000 unique works. In the screenshot above are numbers 7,804, 3,100, 6,965, and 2,140 respectively. Each one can only have one owner, and that ownership is immutable and verifiable on the public blockchain.

Today, many of the NFTs that we see are cartoons like CryptoKitties or abstract art like ArtBlocks, which are easy as adults and professionals to write-off as child-like or irrelevant. But the space Is rapidly evolving day by day with new use cases that have the potential to revolutionize other industries like research, special collections, ebooks, scholarly communications, and more.

Conclusion

At the end of the day, no article, video, or presentation will make things click on the digital economy like participating in it yourself. I would encourage you to get a wallet, secure a .eth domain, and maybe even purchase your first NFT collectible. While I’m learning more about this brave new frontier every day, I’m happy to help if you get hung up along the way.